India’s audit regulations require businesses to comply with various types of audits, governed under different laws. The most common audits are statutory audits, internal audits, secretarial and cost audits under the Companies Act, 2013, and tax audits under Section 44AB of the Income-Tax Act, 1961. Since the commencement of the Goods and Services Tax (GST) law in 2017, businesses and entrepreneurs in India are also required to conduct GST audit each year.

Regulatory framework for financial reporting

- Companies Act, 2013: Mandates that companies prepare financial statements in accordance with prescribed accounting standards and outlines specific requirements for disclosure, consolidation, and presentation.

- Indian Accounting Standards (Ind AS): Aligned with International Financial Reporting Standards (IFRS), Ind AS is mandatory for listed companies, large unlisted companies, and certain public interest entities. Over the years, India has phased in Ind AS to enhance compatibility with global financial systems, increasing transparency for investors.

- SEBI Guidelines: SEBI requires listed companies to follow additional financial disclosure norms to protect investors and maintain market integrity. SEBI’s guidelines ensure companies maintain timely and transparent disclosures, particularly for periodic and quarterly reports, audit committee requirements, and annual reports.

- Institute of Chartered Accountants of India (ICAI): A key regulatory body responsible for setting auditing standards and accounting practices in India, ICAI issues Standards on Auditing (SA) and supports the implementation of Ind AS

- Income-tax Act, 2025: Formally notified by the Central Board of Direct Taxes (CBDT), this new framework came into effect on April 1, 2026, officially replacing the Income-tax Act, 1961. It introduces a modernized tax administration framework with updated definitions, streamlined compliance systems, and enhanced reporting requirements, signaling a decisive shift toward greater transparency, digital integration, and regulatory consistency.

Types of audit

Here we examine each type of audit, what classes of companies are required to conduct it, and penalty for non-compliance.

|

An Overview of Types of Audits under the Companies Act, 2013 |

||||

|

Type of audit |

Scope of audit |

Standards to comply |

Who conducts the audit? |

Who is the report submitted to? |

|

Statutory audit |

Audit of the financial records and statements of the company |

Auditing standards recommended by Institute of Chartered Accountants of India (ICAI) |

A licensed chartered accountant (CA) ; or A cost accountant; or A professional decided by the Board. |

Members |

|

Internal audit |

Audit of the functions and activities of the company |

NA |

A CA (excluding the statutory auditor of the company); or A cost accountant; or A professional decided by the Board |

Board of Directors |

|

Secretarial audit |

|

Auditing Standards recommended by the Institute of Company Secretaries of India (ICSI) |

A practicing company secretary (CS |

Members |

|

Cost audit |

Audit of the cost records of the company |

Cost auditing standards issued by the Institute of Cost and Works Accountants of India |

A practicing cost accountant |

Board of Directors |

Tax audit

The major objective of tax audit are outlined below:

- Ensure proper maintenance and correctness of books of accounts and certifications of the same by a tax auditor;

- To report prescribed information, compliance of various provisions of income tax act;

- Proper books maintenance, calculation, and verification of total income, claim for deductions; and

- Reporting observations/discrepancies noted by tax auditor after methodical examinations of the books of account.

It also verifies if the individual has complied with various requirements of income tax law, such as filing income tax returns, and income tax deductions among others. The tax audit report is submitted along with the income tax return.

Notably, with the transition to the Income-tax Act, 2025 from April 1, 2026, TDS must be reported under Section 393 and TCS under Section 394 for new transactions. Older section references such as Sections 194C, 194J, and others should no longer be used for transactions from that date onward. Transactions completed on or before March 31, 2026 continue to be governed by the Income-tax Act, 1961.

Who needs a tax audit?

A tax audit is applicable to all companies, LLPs, as well as professionals whose turnover crosses a particular threshold limit. Mandatory tax audit limit for different categories of taxpayers:

- Any individual carrying on a business whose sales, turnover, or gross receipts of the business exceeds INR 100 million; or

- Any individual carrying on a professional whose gross receipts exceeds INR 5 million; or

- Any person carrying on a business where the profits and gains from business are lower than the income calculated on a presumptive basis under section 44AE or 44BB of the Income Tax Act; or

- Any person carrying on a business, whose income is lower than the income calculated on a presumptive basis under section 44AD of the Income Tax Act. If the cash transactions are up to 5 percent of total gross payments, the threshold limit of turnover for an audit is increased to INR 100 million.

Businesses registered as MSME (medium, small, and micro enterprises whose turnover is less than INR 50 million (US$611,000) will not be required to undergo a tax audit and carry out less than five percent of their business transactions in cash.

Key auditing standards

| Auditing Standards | Title | Description |

|---|---|---|

| SA 200 | Overall Objectives of the Independent Auditor and Conduct of an Audit | This standard emphasizes the auditor’s responsibility to obtain reasonable assurance that financial statements are free from material misstatement, due to fraud or error. It also highlights the importance of auditor independence and professional skepticism. |

| SA 210 | Agreeing on Terms of Audit Engagements | This standard ensures that auditors and clients mutually agree on the terms of the engagement, thereby defining responsibilities, the scope of work, and reporting expectations. |

| SA 300 | Planning an Audit of Financial Statements | This focuses on the planning of an audit of financial statements. It outlines the auditor's responsibilities in developing an overall audit strategy and detailed audit plan to conduct the audit effectively and efficiently. |

| SA 315 | Identifying and Assessing Risks of Material Misstatement | This standard requires auditors to perform risk assessments and understand the client’s business environment to identify material misstatements. It helps auditors assess where material misstatements could occur. |

| SA 330 | The Auditor’s Responses to Assessed Risks | Outlines procedures auditors should undertake to address the assessed risks, including tests to obtain evidence on the financial statements. |

| SA 500 | Audit Evidence | Emphasizes the need to obtain sufficient and appropriate audit evidence through substantive and control testing to support auditor conclusions. |

| SA 550 | Related Parties | SA 550 deals with the auditor’s responsibilities regarding related party relationships and transactions when performing an audit of financial statements. |

| SA 580 | Written Representations | SA 580 deals with the auditor’s responsibility to obtain written representations from management and, where appropriate, those charged with governance. |

| SA 700 Series (SA 700, 705, 706) | Formation and Reporting of Audit Opinions | These standards guide the formation and reporting of audit opinions. They include requirements on the structure of audit reports and modifications to audit opinions in cases of disagreement or limitations. |

| SA 570 | Going Concern | Requires auditors to assess the entity’s ability to continue as a going concern, identify any material uncertainties, and evaluate their impact on the financial statements. |

Tax audit report

The audit must be conducted by a practicing licensed chartered accountant (CA). The auditor must submit the tax audit report in the following format:

- Form 3CA: When a company is already mandated to get their accounts audited under any law. This is applicable to companies that get their accounts compulsorily audited under the Companies Act, 2013; or

- Form 3CB: When a company or individual gets their accounts audited under the section 44AB of the Income Tax Act.

Further, the tax auditor must submit Form 3CD along with either of the above-mentioned forms, as it is a part of the audit report.

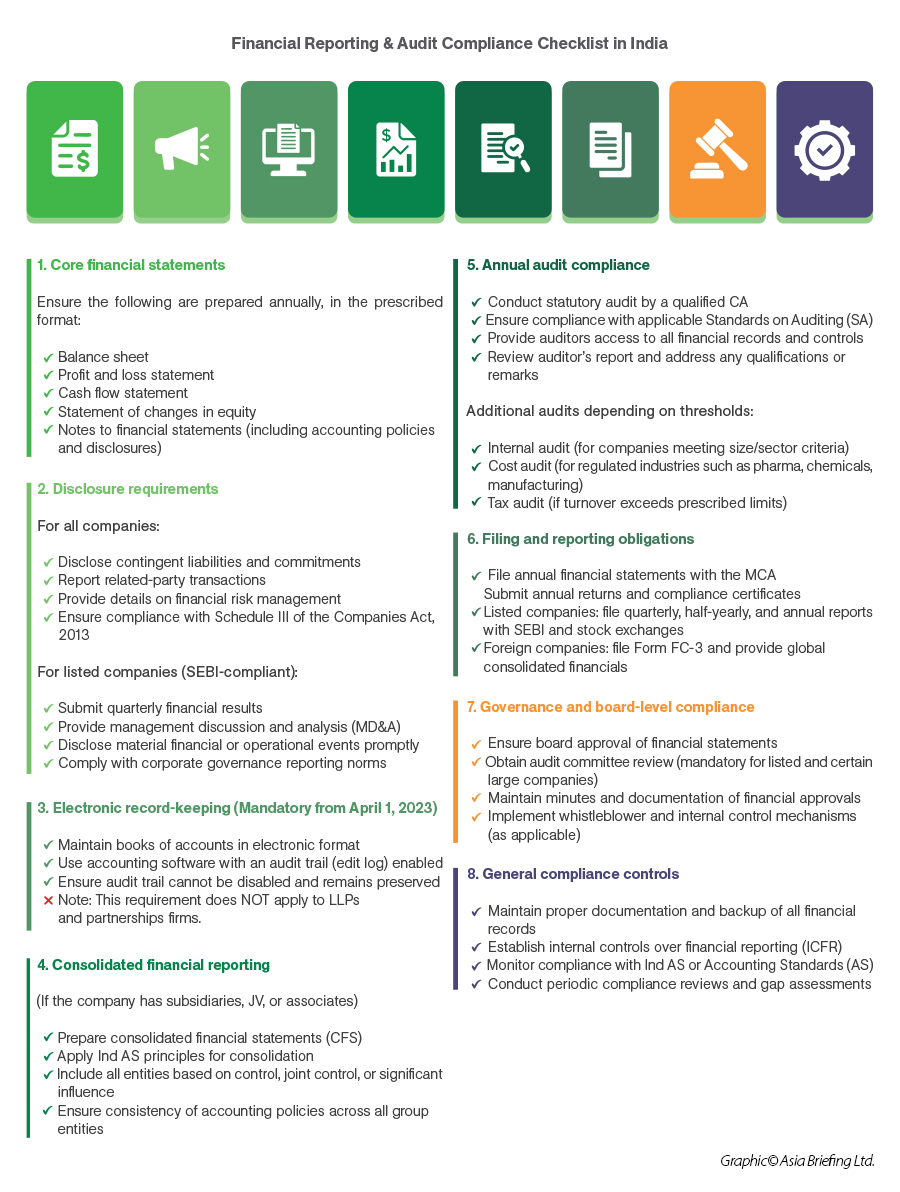

Financial statement requirements and disclosure norms

Indian companies are required to prepare a range of financial statements, including:

- Balance sheet: Provides an overview of the company’s financial position, showing assets, liabilities, and shareholders’ equity.

- Profit & loss statement: Details revenue and expenses, providing insight into profitability over a financial year.

- Cash flow statement: Reflects cash inflows and outflows, critical for assessing liquidity.

- Statement of changes in equity: Shows changes in equity, including profits, losses, dividends, and adjustments.

- Notes to financial statements: Additional disclosures, including accounting policies, contingent liabilities, risk management practices, and related party transactions.

For listed companies, SEBI mandates quarterly disclosures of financial results, adherence to certain minimum benchmarks, and disclosure of any significant financial and operational changes. Non-listed companies are typically required to disclose only annual financials unless they fall under specific public interest criteria.

India has seen significant digitalization in the reporting and auditing process. Technologies like blockchain, artificial intelligence (AI), and data analytics are increasingly used to ensure accuracy, reduce human error, and detect fraud.

Additionally, the Ministry of Corporate Affairs’ MCA21 platform allows companies to file statutory documents electronically, facilitating easier regulatory compliance. The MCA requires companies to submit financial data in XBRL format, improving data comparability and analysis for regulatory authorities.

The MCA’s portal, coupled with digital signatures and electronic submissions, simplifies the reporting process and enhances transparency. Cybersecurity audits are also becoming critical as companies face rising cyber threats, requiring auditors to assess controls and risk management frameworks.

Under the Income-tax Rules, 2026, companies are now also required to maintain shareholder registers within India, conduct annual general meetings domestically, and ensure dividend payments are made only within India, reinforcing domestic regulatory oversight. Furthermore, recognized stock exchanges face stricter compliance conditions, including mandatory SEBI approval, maintenance of detailed client information such as PAN and unique IDs, preservation of transaction audit trails for seven years, and submission of monthly reports on modified transactions.

Risk assessment, internal controls, and fraud detection

For listed companies, reporting on internal financial controls is mandatory, ensuring stronger risk oversight. SA 240 addresses fraud risks specifically, requiring auditors to monitor high-risk areas like revenue recognition and related-party transactions to prevent misstatements.

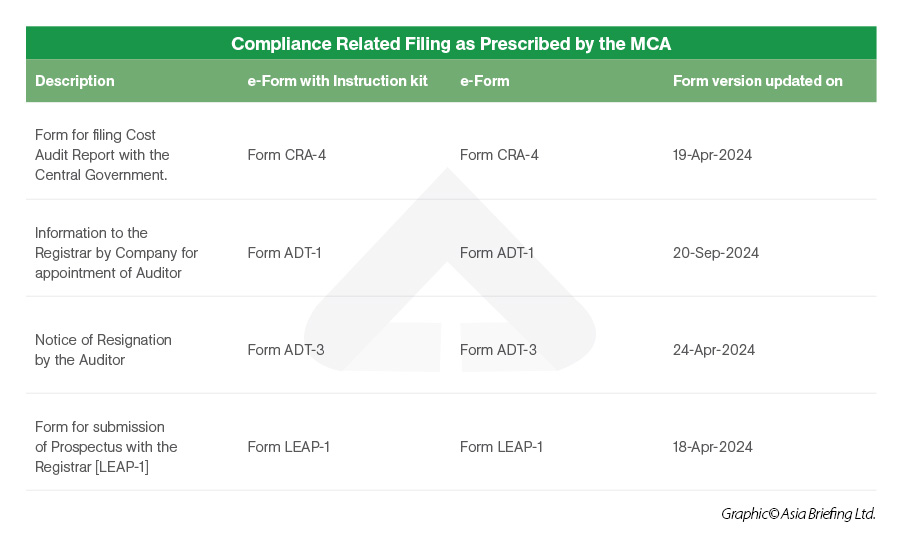

In India, financial reporting requirements for different types of entities are governed by relevant statutes. A brief summary of this is given below:

.jpg)

Penalty for non-compliance

If a company or an individual is not in compliance with the tax audit provisions, or fails to conduct a tax audit, then a penalty of 0.5 percent of total sales not exceeding INR 1,50,000 is imposed.

Businesses must also be mindful of ongoing compliance deadlines within a financial year. During April and May, the opening months of FY 2026-27, companies must simultaneously conclude compliance obligations for the previous financial year while beginning to align with new reporting requirements for current transactions under the Income-tax Act, 2025.

Key milestones during this period include:

- Depositing TDS/TCS for April 2026 by May 7;

- Issuing TDS certificates for March 2026 and submitting the quarterly TCS return for Q4 (January–March 2026) by May 15; and,

- Filing the quarterly TDS return for Q4, as well as other key annual forms such as Form 61A (statement of financial transactions) and Form 61B (reporting of financial accounts) by May 31.

Managing a GST audit

The GST system requires taxpayers to self-assess their tax liability and pay their tax without any intervention by the tax authorities. The law provides for a robust audit mechanism to measure and ensure compliance by the taxable person.

The GST audit checks the accuracy of information furnished, taxes discharged, refund claimed, and input tax credit availed by the individual taxpayer.

As per changes introduced to the GST audit norms by the Finance Act, 2021, any registered taxable person whose annual aggregate turnover exceeds INR 50 million during a financial year needs to get their accounts audited.

Furthermore, the compulsory GST audit requirement by a Chartered Accountant or a Cost and Management Accountant for taxpayers with a turnover exceeding INR 20 million stands removed. The Form GSTR-9C is to now be self-certified and submitted by taxpayers with a turnover of more than INR 50 million from FY 2020-21 onwards.

|

Turnover |

GSTR 9: Annual return to be filed yearly by taxpayers registered under GST |

GSTR 9C: Certified copy of the audited annual accounts and a reconciliation statement |

|

Up to INR 20 million |

Optional |

Not Applicable |

|

INR 20 million - INR 50 million |

Mandatory |

Optional |

|

Above INR 50 million |

Mandatory |

Mandatory (can bbbe filed through self-certification, no professional required |

Items included to calculate turnover:

- All taxable (inter-state and intra-state) supplies other than supplies on which reverse charge is applicable;

- Supplies between separate business verticals;

- Goods supplied to/received from job worker on principal basis;

- Value of all export/zero-rated supplies;

- Supplies of agents/ job worker on behalf of the principal;

- All exempt supplies. For example, agricultural inputs, such as produce, that is supplied along with branded ready-to-consume food; and

- All taxes other than those covered under GST, such as entertainment tax paid on the sale of movie tickets.

Items excluded when calculating the turnover

- Inward supplies on which tax is paid under reverse charge;

- All taxes and cess charged under the GST, that is, the CGST and SGST or IGST, Compensation Cess;

- Goods supplied to or received back from a job worker; and

- Activities that cannot be categorized as supply of goods or service under schedule III of the CGST Act.

Filing GST audit

To file the audit, the taxpayer must submit the following documents electronically:

- An annual return using the form GSTR-9 by December 31 of the next financial year;

- A copy of audited annual accounts;

- A certified reconciliation statement in the form GSTR-9C, reconciling the value of supplies declared in the return with the audited annual financial statement; and

- Any other particulars as prescribed under the law.

In this category of audit, the government prescribes different types of annual return: GSTR-9 is for regular taxpayers and GSTR-9A is for composition scheme.

Taxpayers must note that the annual return is applicable to all registered persons in GST except input service distributors, casual taxable persons, non-resident taxable persons, and persons liable to deduct tax at source.

For the reconciliation statement, it is advisable for GST registered entities to have a copy and maintain their accounts as a proof to show correctness with regard to the following:

- Production of the goods (taxable inward supply of goods and/or service or both taxable outward supply of goods and/or services or both);

- Stock of goods;

- Input tax credit availed; and

- Output tax payable and paid.

GST compliance for digital services: OIDAR

A growing area of GST compliance relevant to businesses in India involves Online Information and Database Access or Retrieval (OIDAR) services.

Under India's GST framework, OIDAR refers to digital services delivered over the internet or electronic network that are essentially automated and involve minimal human intervention. India taxes these services based on the location of the recipient, meaning foreign providers can trigger GST liability simply by serving Indian users.

Services covered under OIDAR include:

- Cloud computing and SaaS platforms;

- Digital advertising and data services;

- Streaming services;

- E-learning platforms;

- Online gaming;

- Supply of e-books;

- Software and digital downloads;

- Data storage and hosting;

- AI tools and APIs; and,

- Subscription-based digital memberships.

Services involving significant human intervention, such as consulting, advisory, or live training, are generally excluded from OIDAR classification.

A central concept in determining GST liability under OIDAR is the Non-Taxable Online Recipient (NTOR) — a person located in India who is not registered under GST and receives OIDAR services for non-business (personal) purposes. For business-to-consumer (B2C) supplies to NTORs, the foreign service provider is required to register under GST in India, charge and remit GST, and file returns under GSTR-5A. For business-to-business (B2B) transactions with GST-registered recipients, the tax liability typically shifts to the Indian recipient under the reverse charge mechanism.

For foreign entities supplying OIDAR services to NTORs in India, GST registration is mandatory from the first transaction, regardless of turnover. No threshold exemption applies. Once registered, OIDAR providers must file a monthly return under FORM GSTR-5A, due by the 20th of the following month, covering B2C supplies to Indian consumers and tax payable. GST must be paid in Indian Rupees, and no input tax credit mechanism is available for foreign OIDAR providers.

General GST audit

In general GST audit the commissioner or any other officer authorized by the commission may undertake the audit of any registered individual for such period, at such frequency, and in such manner as prescribed under the GST law.

The audit may be conducted at the place of business of the registered person or in the office of the commissioner or officer authorized by the commissioner.

The time-frame for carrying out the audit is three months. The officials serve registered taxpayers an advance notice at least 15 days prior to the audit commencement. Starting from this day, the audit must be completed within three months. In special cases, the authorized officer can extend the time-period for audit completion by not more than six months.

During the course of GST audit, the authorized officer may require the registered person to:

- Provide the necessary facility to verify the books of account or other documents as required; and

- Furnish such information as required and render assistance for timely completion of the audit.

Special GST audit

Special audits are audits ordered by a GST Officer and conducted by a Chartered Accountant or CMA. An assistant commissioner of the GST can order a GST special audit when he/she suspects that the assessee declared taxable values incorrectly or provided the utilized input tax credit inappropriately. These disparities may include:

- Incomplete audit;

- Discrepancies observed in the liability with the intention to evade tax; and

- Incorrect revenue declaration.

The officer orders a special audit through Form GST ADT-03 and the taxpayer should audit the accounts after or before the commencement of any scrutiny, enquiry or investigation. The GST Officer shall select the CA or CMA to perform the audit and the taxpayer should cooperate with the Auditor for completion of the audit.

Once the audit is complete, the CA or CMA would submit the findings of the audit in Form ADT- 04. A special audit must conclude by an auditor within 90 days. In rare cases, the due date may extend to another 90 days by the Commissioner, based on an application made by the CA or CMA.

On conclusion of a special audit under GST, the taxpayer is provided with an opportunity to be heard in respect of any material gathered in the special audit which is proposed to be used in any proceedings against the taxpayer.

How to prepare for the GST audit and annual return filing

Companies that have a presence in multiple locations, in the form of a subsidiary or branches across the country, must compute annual turnover on an all India PAN basis. The GST Law treats every entity of a company located in more than one state or union territory as distinct.

If the entity is registered in more than one state or union territory, and the aggregate turnover from all such states exceeds INR 50 million, then the entity must get state-wise accounts audited under the GST law.

Aggregate turnover includes the value of all exempt supplies and exports under the same PAN, on an all-India basis. In cases, where companies have multiple GSTIN state-wise registrations on the same PAN, traders and dealers must internally derive their turnover GSTIN-wise and declare the amount in Form GSTR-9C.

Companies that have multiple registrations within the state must maintain separate accounts as the law requires companies to file a reconciliation statement separately for each (GSTIN) registration within the state.

FAQ:Common Compliances for Companies in the Indian Regulatory Landscape

What are the challenges companies face while ensuring that necessary regulatory compliances are completed?

Managing compliances in today’s highly complex economic and regulatory environment is no easy task. Companies face many challenges, including:

- Rapid globalization;

- Ongoing developments in tax and other allied laws;

- Changes in accounting standards;

- Increased demand from regulatory authorities for greater transparency and cooperation;

- Acute shortage of qualified professionals;

- Obtaining accurate data in an efficient manner;

- Global trends towards centralization of compliances; and

- An ever-evolving technology ecosystem.

Businesses must additionally navigate the transition to the Income-tax Act, 2025, which requires alignment with updated section references, new valuation frameworks for capital assets and fair market value, and expanded provisions on non-resident taxation and significant economic presence, all of which add layers of complexity to compliance management.

Can you list a few common laws and legislations that are applicable to companies in India?

The following laws are applicable to companies in India:

- The Companies Act 2013 and Rules thereof;

- Labor and Employment Laws;

- Environmental Laws; and

- Tax and Stamp Duty.

Can you explain the scope of compliances under Companies Act, 2013?

The scope of compliances under the Companies Act covers but is not limited to the following:

The Companies Act, amongst other provisions, lays down detailed guidelines regarding qualification and appointment/ removal of directors, retirement of directors, their remuneration, passing board resolutions, arranging board and shareholders meetings, oversight on related party transactions, timely maintenance of books of accounts and the preparation and presentation of annual accounts (matters that must be included in the annual reports of the companies), filing of forms with the Registrar of Companies periodically, etc.

Subsequent to the completion of all legal formalities required for incorporation, and the issuance of the certificate of incorporation, the company is recognized as a separate legal entity in the eyes of the law, distinct from its members who have incorporated the entity.

Whether it is a private or a public company, various things are supposed to be dealt with post incorporation. There are matters that must be undertaken in the first board meeting immediately post incorporation, and then there are tasks that are required to be carried out on a periodical basis.

A company conducts its business through its Directors who are accountable in the event of failure to comply with the above compliances.

Soon after a company is incorporated, but no later than 30 days, an appointed director is under obligation to call the First Board Meeting by issue of notice (together with the agenda) of the meeting at least seven days prior to the meeting. Several important matters need to be resolved in this first board meeting.

A company must also place its sign board outside the registered office address, with its name, registered office address, company identification number, e-mail ID, and phone number (mandatory fields as per the current mandate), Website address and fax number, if any, stated on it. These details must also be printed on all business letters, billheads, and all other official publications.

As mentioned under section 173(1) of the companies act of 2013, a company must convene at least four board meetings, in addition to the first board meeting, with a gap of no more than 120 days between two consecutive board meetings in a calendar year. Detailed minutes of the meetings should be prepared, recording the important actions taken by the Board of Directors and the same must be maintained as a permanent document by the company. Within 30 days from the meeting, the minutes must be prepared, duly signed, and maintained in a minute’s binder.

Similarly, on allotment of shares, the company must issue share certificates to those who have been allotted the shares and must maintain both a members register and a shares allotment register. A company is also required to file various financial statements along with the auditor’s report and annual return before the due date every financial year with the Registrar of Companies.

Additionally, there are several instances wherein a company has to intimate the concerned Registrar of Companies, on a timely basis, about the appointments/ removal of directors and certain other changes in a prescribed manner.

The above-mentioned compliance requirements under the Companies Act is not an exhaustive list. Some companies may also be required to ensure several other additional compliances such as registration under the GST, Professional Tax, and Shops and Establishment Act. It is important to understand that the responsibility of complying with the central and state by-laws is indeed, a continuous process.

What is the scope of compliances under Labor and Employment Legislation?

For ensuring workers’ right to minimum wages, the Central Government has amalgamated 4 laws in the Wage Code, 9 laws in the Social Security Code, 13 laws in the Occupational Safety, Health and Working Conditions Code, 2020 and 3 laws in the Industrial Relations Code. By getting these Bills passed in the parliament, the Central Government has made significant headway in changing the standard of living of workers.

These labor reforms will enhance ease of doing business in the country. Employment creation and output of workers will also improve. The benefits of these four Labor Codes will be available to workers in both the organized and unorganized sector. Now, the Employees’ Provident Fund (EPF), Employees’ Pension Scheme (EPS) and coverage of all types of medical benefits under Employees’ Insurance will be available to all workers.

Companies must put consistent effort to ensure that proper compliance of these various statutes vis-à-vis the working condition for its employees are in order, and that the HR policies are formulated in accordance with the guidelines mentioned in the central and state by laws.

What is the scope of compliances under Environmental Laws?

The scope of compliances under Environmental Laws covers, but isn’t limited, to the following:

Environmental and pollution control matters fall under the ambit of various statutes such as:

- The Environment (Protection) Act, 1986;

- The Water (Prevention and Control of Pollution) Act, 1974;

- The Air (Prevention and Control of Pollution) Act, 1981;

- Hazardous Wastes (Management, Handling and Trans boundary Movement) Rules, 2008;

- The Manufacture, Storage, and Import of Hazardous Chemicals Rules, 1989;

- The Indian Forest Act, 1927;

- The Forest (Conservation) Act, 1980;

- The National Environment Tribunal Act, 1995; and

- The Public Liability Insurance Act, 1991, etc.

Companies are required to comply with the provisions of these environmental laws to the extent specifically applicable to their business operations. The consequences of non-compliance with the provisions of any such statutes and rules are provided in the respective statutes.

What is the scope of compliances under Tax and Stamp Duty related laws?

The scope of compliances under the Tax and Stamp Duty related laws covers, but is not limited, to the following:

There is a federal tax structure in India and taxes are levied by both the Central and State Governments, along with other local regulatory authorities. These taxes are broadly classified as:

- Direct Tax (which includes income tax, minimum alternate tax (MAT), share buy-back tax),

- Indirect Tax (which includes GST, Excise Duty, Customs Duty, Entry Tax, R&D Cess), and

- Charges on transactions (including stamp duty, securities transaction tax, and commodity transaction tax).

All Indian companies are subjected to payment of tax and stamp duty for their business transactions undertaken during any financial year and on the income generated from such operations. Delayed/ non-payment and inadequate payment of tax and stamp duty may attract moderate to heavy penalties, cause enforceability issue of the documents and, in some cases, impounding of the documents by the authority.

Apart from the ones mentioned above, are there any other enactments that are applicable for companies in India?

Whilst the above explained laws and enactments lays down the general laws governing a company in India, local state laws also play a very important role. Therefore, the need for companies to be mindful of adhering to local state laws in which they are registered and conducting their business must not be overlooked.

What are the consequences of non-compliance of the provisions of Acts and Enactments as mentioned above?

The policy and procedures regulating, and governing Indian corporations have been progressively liberalized and simplified over the last few years. However, there are several compliance mandates that must be adhered to, failure to do so could trigger various compliance risks such as disqualification of directors, attracting of penal provisions and in some cases even imprisonment of the directors and key management personnel.

What is compliance risk and how can companies manage it?

Compliance risk refers to an exposure to legal penalties, financial forfeiture, and the material loss an organization faces when it fails to act in accordance with industry laws and regulations, internal policies, or prescribed best practices. Compliance risk can also be referred to as integrity risk. Several compliance regulations are enacted to ensure that companies operate ethically and in a fair manner.

Compliance risk management constitutes the widely known collective governance, risk management, and compliance (GRC) discipline. The three fields have been known to overlap frequently in the areas of internal auditing, incident management, operational risk assessment, and compliance with regulations such as the Sarbanes-Oxley Act of United States. Penalties for compliance violations include payments for damages, fines, and voided contracts, which can lead to a loss of reputation and business opportunities for organisations, as well as devaluation of its franchises.